Business strategy is a fuzzy discipline, as literature boasts several separate schools of thought and dozens of definitions (1).

Quoting F. Frey (2) (professor at ESPC-EAP European School of Management in Paris), business strategy comprises three objectives:

No wonder that strategy, with its resource planning, development of unique competencies and management systems, utilising emerging technologies and adoption to the changing environment, gets sometimes confused with microeconomics, finance or marketing.

Alignment of your thought process with the 3 objectives below in mind is a helpful framework as a starting point.

Firstly, businesses’ ability to create sustainable value , is the ultimate goal from the perspective of customers, investors and shareholders.

So what is the value your business creates, can be defined by asking yourself these questions:

Secondly, creating value without innovation gets difficult, if not impossible. Each Leadership Team aspires for their organisation to build its competitive advantage (3) and forge the ability to prevent, implement or leverage imitation. Extensively adopted ESG (4), ISO (5), Six Sigma system (6), etc. are for the customers’ and investors’ threshold requirements rather than distinctive practices.

Today, availability of office software, systems and equipment is widely accessible and affordable moreover, there are business applications available free of charge. What is truly setting you apart from your competition are the unique skills (7) and capabilities of your workforce (8), as well as your recruitment process set to attract the right talent for your business and its culture talent.

Hence the importance of creating culture of trust and collaboration to foster divergent ideas contributing to successful execution of your business strategy.

Finally, for successful execution, each organisation needs to define its operating perimeter – scope (the business you are in) and position along the value chain order to prevent value migration.

What if your business was a ship?

If you compare managing your business to navigating a ship, your operating perimeter is the type of vessel you operate (what it can/cannot do), your direction comes from your destination point which you aspire to reach (your vision) and whilst you sail you need to take into account external and internal factors and forces (within and outwit your control e.g. wind, currents, etc., which are business equivalent to regulatory requirements, technology advancements, competitive pressures and other challenges, such as: like inflation, pandemics, etc.) to define the best route to reach your end goal.

The wind impacts your direction, forcing you off your target. This requires skills of your team to make informed decisions and get back on track.

Your decisions may concern:

Senior executives put pressure on their teams to come up with accurate projections regarding market evolution, customers’ behaviours and competitors’ responses thinking that forecast precision is the key to defining winning strategies (9). Attempting to develop precise forecasts in the age of volatility is fool’s errand, which will cost time, effort, and energy with dubious results.

Today, global challenges such as: geopolitical unrest, energy uncertainty, surging inflation, supply chain disruption, global health issues, etc., all happening at once, have increased challenges to a level never witnessed by management teams.

Therefore, instead of trying to project the unknowns, assess effectiveness of your decisions. Are you set on the right trajectory to get back to the course toward your destination? Use tangible targets, milestones, and metrics reviewed frequently to verify the position and coordinates of your course.

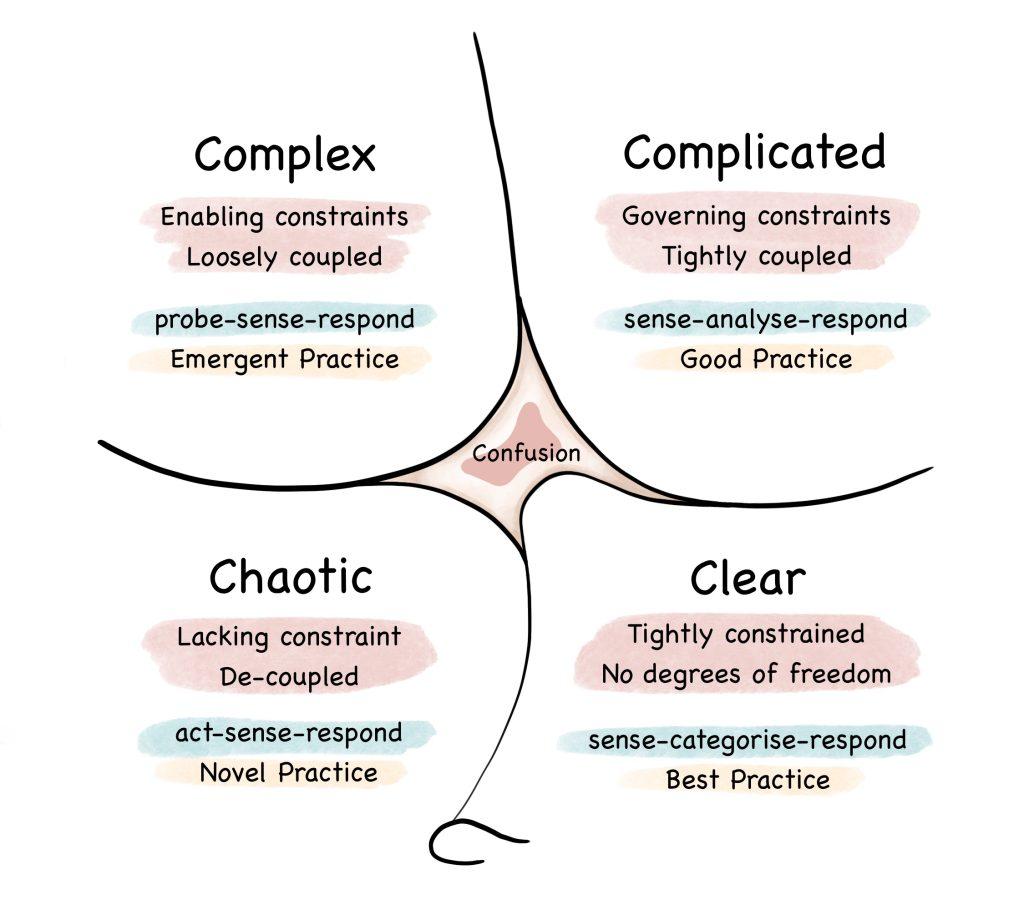

To avoid analysis paralysis in the times of uncertainty and volatility, you may refer to the Cyrefin’s Framework (10), designed to support our assessment of a situation and help us selecting the best response in case our preferred management style fails.

The Cyrefin’s Framework distinguishes 5 decision-making environments (known as contexts), which are defined by cause and effect relationships. The first four contexts: clear, complicated, complex and chaotic, require leaders to diagnose a situation and act in contextually appropriate way. The last one – confusion, requires a different approach, whereby we take a step back, gather more intel in order to get more clarity as to the predominant context.

What questions remain relevant?

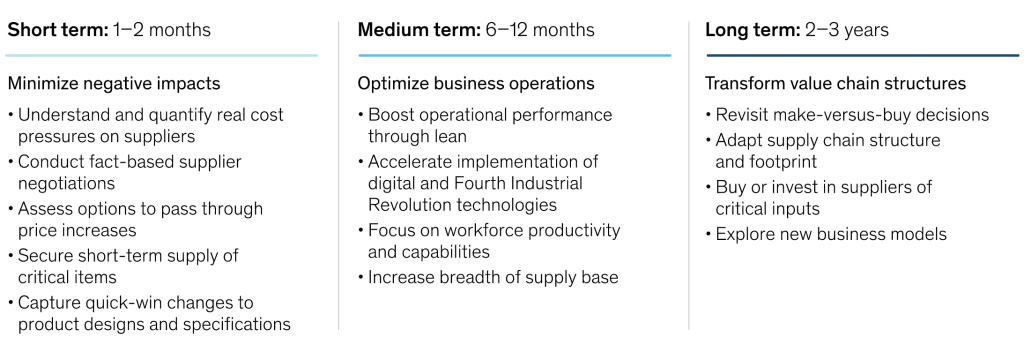

To remain competitive in current circumstances, organisations and their management team must be able to move quickly and translate business strategy into a set of priorities, such as per the example provided by McKinsey below (11).

This requires non-conventional wisdom beyond traditional data analysis (12), which according to McKinsey, comes from diversity, collaboration with other businesses and perspective from disruptors across industries, asking questions such as:

Rolling these priorities out requires different parts of the business to collaborate and move in tandem. In traditional organisations strategic priorities are rolled out from the top down and reviewed annually.

This process is time-consuming and in reality undermines the alignment, coordination and agility, which is required by a business to execute its strategy in uncertain and volatile times.

If you are ready to consider options not explored before, look at three, non-exclusive recommendations I make below. To make sure you are on the right track evaluate them in terms of fit for purpose to your business using a Six Sigma tool known as impact matrix (13).

1. Invite your talent to join you on this journey

In the age of volatility, transparency of targets across the organisation fosters agility and adaptability to changing circumstances.

Instead of resorting to time-intensive process of cascading goals down the chain of command (14), the whole organisation sees and understands top-level objectives allowing for fast alignment with the company’s direction, required to get ahead of events rather than react to them.

“If you want to build a ship don’t drum up the people to gather wood and give orders. Instead teach them how to yearn for the vast and endless sea.”

ANTOINE DE SAINT—EXUPERY

Flexibility of manoeuvre, ability to alter strategy and priorities in the face of extreme volatility is a unique capability. Even if defining an exact path is extremely difficult, great performance (15) still requires a direction. This is why the conservative and hierarchical process of cascading priorities down the chain of command fails and requires replacing with a dynamic decision-focused approach cut for today’s challenges.

If your team is self-motivated, believes (16) in doing the right thing quickly, but not rushed, is self-awareness to ask questions when not sure – you don’t need to micromanage them. Otherwise, you may want to set targets to measure performance of your employees. There are few schools of thought to select from.

“Measurement by objectives” has been introduced by Drucker in the 50’s and repackaged in the 80’s by Goran as SMART goals (specific, measurable, achievable, realistic and time-bound). The more recent mutations are FAST and PACT goals (17).

FAST stands for:

Whereas the PACT acronym stands for:

If you decide that any of the target-setting methodologies are for you, please remember to set an expected timescale.

“A goal without a deadline is just a dream.”

ROBERT HERJAVEC

2. Re-think products & service offering for value

Our design choices for products and services are key response to the volatility of commodities, scarcity of raw materials and components, and growing cost base.

These choices are not to compromise core functionality but to improve cost baseline, address customers’ needs and strengthen business offering in a sustainable way.

To achieve this, mobilise cross-functional expertise to identify design optimisation and implement alternative solutions (18):

This approach will require not only internal functions (product managers, functional engineers, etc.) to work together, but also customers and supply chain representatives to contribute with ideas and suggestions for well-rounded solutions.

3. Re-imagine procurement to create value, not just cut cost

Finally, I recommended re-inventing procurement due to the fact, that increased transportation, energy and materials cost impact not only working capital but also customers’ behaviour (19).

You may want to start with these steps:

There are other aspects that will require your consideration, such as customers’ willingness to pay premium to ensure availability of goods or suppliers’ agreement to share cost in order to lower the risk of disruption in demand for their products.

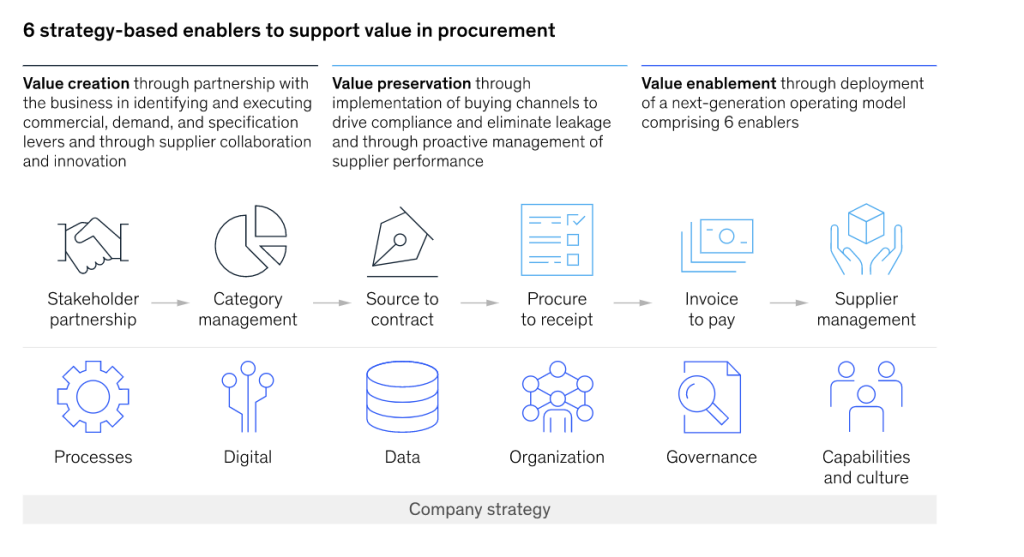

If you haven’t done that yet, you may want to empower your Head of Procurement to raise the bar on value-creating contributions of your procurement organisation.

I have included McKinsey’s diagram for your interest and to guide you through the possible sources of value.

Source: McKinsey & Company: “Responding to inflation and volatility, time for procurement to lead” (Jul 19, 2021)

Source: McKinsey & Company: “Responding to inflation and volatility, time for procurement to lead” (Jul 19, 2021)This blog provides practical guidance and helpful tools to kick off and navigate through the process of improving your business strategy, should you decide this is required. Based on experience, cost of inaction can be higher and more severe than attempting and learning from mistakes.

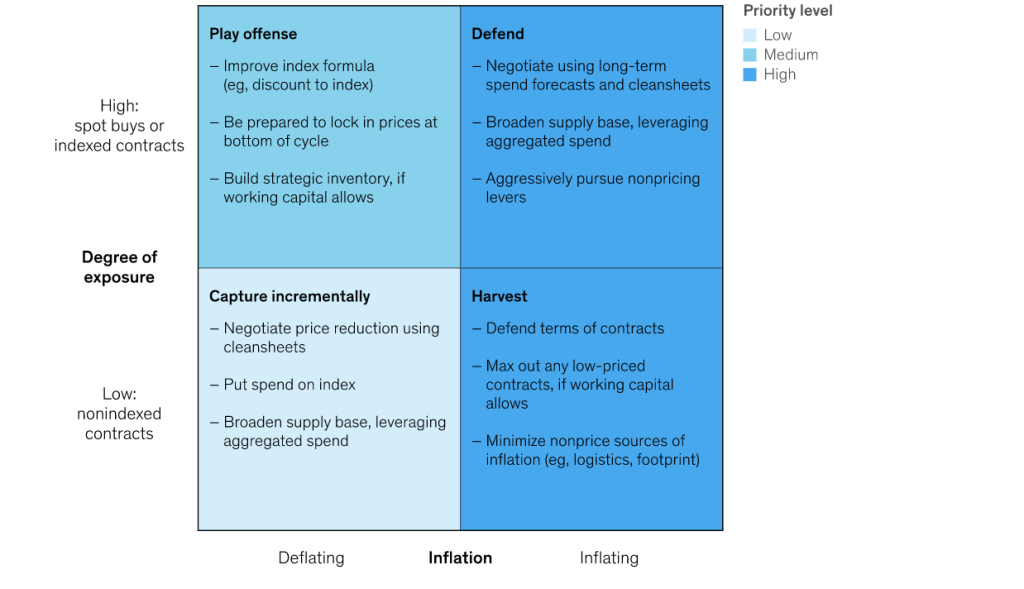

There are schools which suggest various strategies to deal with exposure and inflation in the age of volatility – see below.

Regardless of your approach to deal with the volatility, none of my recommendations above is possible without the right people supporting your efforts.

Therefore, before you embark on the journey to enhance your business strategy and roll out business priorities, consider your business culture, the type of professionals which your organisation attracts and the level of diversity driving creative ideas.